Auto finance loans is a managed LP collateral approach for DeFi borrowing

Auto finance loans is a DeFi borrowing page focused on using managed liquidity provider positions as collateral while automated strategies keep capital active in yield markets. The core idea is simple: liquidity sits in AMM pools, a management layer adjusts positions across DeFi venues, and the borrower uses that productive position to support a loan instead of leaving collateral idle in a wallet.

This topic belongs at the overlap of automated yield farming, liquidity management, and collateralized borrowing. Auto Finance describes its broader product as automated DeFi yield farming and liquidity management, so the loan angle is about how that managed liquidity position fits into borrowing decisions. A user is not merely picking a lending market; the position being pledged has its own fee income, reward flow, price exposure, and liquidation behavior.

LP collateral changes the shape of a crypto loan

A standard crypto loan starts with a single asset deposit such as ETH, BTC-wrapped liquidity, or a stablecoin. LP collateral is different because the position represents a share of a trading pool. Its value moves with the underlying pair, its fee accrual follows swap activity, and its composition changes as traders move the pool price. Auto finance loans makes sense for users who already understand that a pool token is an active market position rather than a static balance.

The borrowing side still revolves around familiar DeFi mechanics: collateral value, loan-to-value limits, interest accrual, and liquidation thresholds. The distinctive part is that the collateral is tied to liquidity management. When an automated strategy narrows, widens, migrates, or rebalances a position, the borrower's risk profile changes with the new pool exposure.

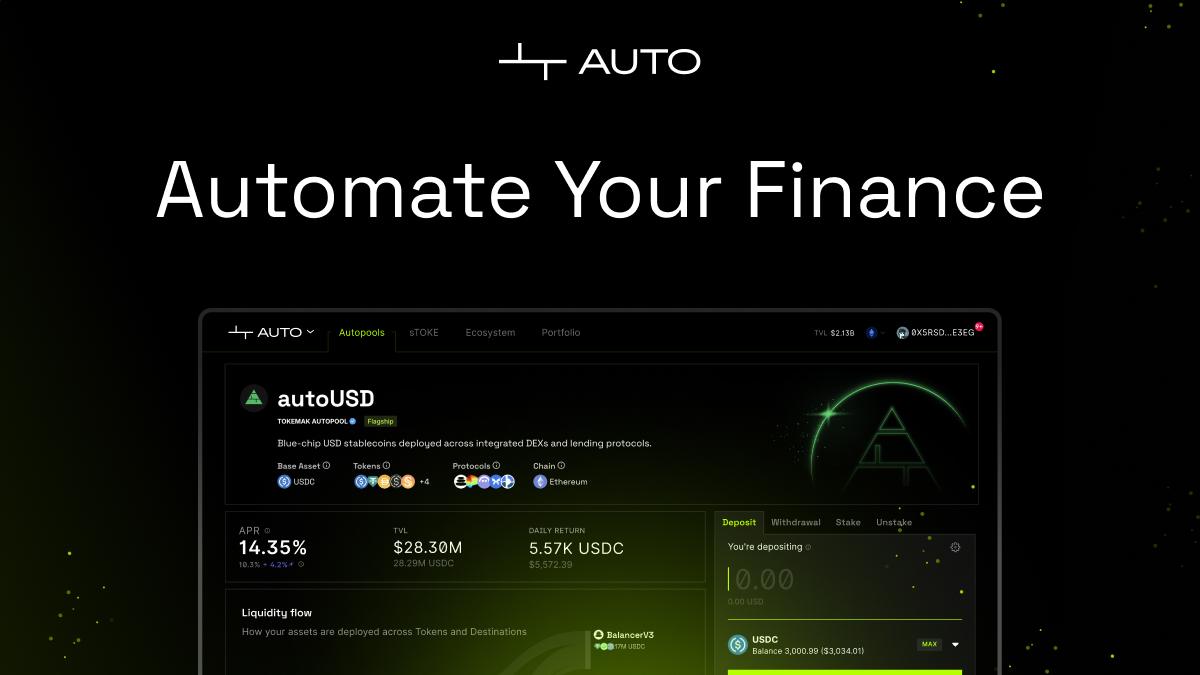

How managed liquidity supports loan collateral

Managed liquidity starts with a strategy that allocates assets into one or more AMM pools. In concentrated liquidity systems, the strategy sets price ranges; in broader pool designs, it decides which pair or pool best matches the risk and expected fee environment. The management layer tracks pool conditions and adjusts the position so idle capital is reduced and fee capture remains aligned with the chosen strategy.

When that managed position backs a loan, the system treats the LP position as collateral with a changing market value. Fees and farming rewards improve the position's economics, while adverse price movement and impermanent loss reduce it. Auto finance loans therefore links two calculations that users normally evaluate separately: expected borrowing cost and expected liquidity yield.

That connection is powerful because the same capital has two jobs. It backs a debt position while remaining deployed in DeFi liquidity. It also adds complexity, since the collateral's value depends on pool prices, smart contract execution, reward emissions, and strategy rules.

What the borrower watches after opening a position

After a loan is open, the most important screen is the health of the position. The collateral ratio tells the borrower how much room remains before liquidation, while the loan balance shows interest accumulation over time. For Auto finance loans, the LP side adds extra signals: pool composition, accrued fees, claimable rewards, and whether a strategy has rebalanced into a different range or pool.

- Collateral ratio and liquidation price for the debt position.

- Current value of the LP position after price movement.

- Borrow rate, repayment amount, and accrued interest.

- Pool fees, incentive rewards, and strategy performance.

- Withdrawal rules that affect repayment or collateral release.

These numbers matter together. A high-yield pool with unstable assets creates a different loan profile from a stablecoin pool with lower fees. The borrower is choosing a combined structure, not a standalone yield vault and a separate credit line.

Where the yield comes from while collateral stays deployed

Yield in this setup comes from liquidity provider economics. Traders pay swap fees to the pool, and LPs receive a share according to the pool design and their liquidity share. Some pools add token incentives from protocols that want deeper liquidity. Automated liquidity management directs capital toward pools and ranges where fee capture and incentive rewards match the strategy's risk boundaries.

Auto finance loans is strongest as a concept when the yield side is transparent enough to compare with borrowing costs. If a position earns fees in the same asset used for repayment, accounting is straightforward. If rewards arrive in volatile tokens, the borrower has a second market exposure. The loan is still measured against collateral value, while the yield stream arrives through pool mechanics rather than a fixed coupon.

Opening a loan against a managed LP position

The workflow begins with assets that fit the chosen pool. A user supplies the pair, deposits into the managed liquidity strategy, and receives a position whose value is tracked by the protocol interface. From there, the loan terms show how much borrowing capacity that position supports. The conservative move is to borrow below the maximum and leave room for pool volatility.

Once the debt is drawn, repayment works like other collateralized DeFi loans. The borrower sends back the borrowed asset plus interest, then releases or unwinds the collateral after obligations are settled. If accrued fees or rewards are available, they become part of the position management decision: harvest, compound, sell for repayment, or leave the strategy running.

In practice, Auto finance loans also raises a timing question. Entering a pool during fast price movement exposes the collateral to rapid composition changes. Borrowing after a strategy has stabilized in its target range gives the user a clearer starting point for collateral health.

Stable pools, volatile pairs, and collateral quality

Collateral quality is not identical across LP positions. Stablecoin pairs have simpler price behavior, though they still carry protocol and asset risk. ETH-stablecoin or BTC-stablecoin pools add directional exposure because the pool shifts as the crypto asset rises or falls. Long-tail token pools deliver larger fee opportunities in active markets, but they bring thinner liquidity and sharper drawdowns.

That distinction affects how a lender values the collateral. A managed position in a deep stable pool supports a different loan limit than a volatile pool built around a new token. Auto finance loans should be read through that lens: the strategy behind the LP position matters as much as the borrowed amount.

Risks that belong to LP-backed borrowing

The main risk is liquidation caused by falling collateral value or rising debt. LP-backed borrowing also includes impermanent loss, reward-token volatility, smart contract exposure, oracle design, and strategy execution. One specific caution belongs here: borrowing near the maximum against a volatile LP position leaves little time to react when pool prices move quickly.

Notably, Automation reduces manual work, yet it does not remove market exposure. Rebalancing adjusts where liquidity sits; it does not erase the impact of price movement. Fee income offsets some losses during active trading periods, but fee income is variable, and the debt balance keeps accruing until repaid.

Aave, Compound, and vault lending as alternatives

Users comparing this approach with established DeFi lending markets should separate collateral type from borrowing venue. Aave and Compound are known for overcollateralized lending against listed assets, with rates set by market utilization. They are simpler when the goal is borrowing against a single token and monitoring a health factor without LP strategy variables.

Vault-style yield platforms focus on automated compounding and strategy execution, while DEX LP managers focus on fee capture and range management. Auto finance loans combines those concerns with borrowing, which makes it attractive to users who want productive collateral and less attractive to users who only want the cleanest debt position. The best fit is a borrower who already accepts LP risk and wants the position to support liquidity needs without fully exiting the pool.

Reading the page like a DeFi borrower

The useful way to evaluate this page is to map the full cash flow. Assets enter a liquidity strategy, the LP position receives fees or rewards, the position supports borrowing, interest accrues on the debt, and collateral health changes with pool value. Each step has a number that belongs in the borrower's calculation.

Typically, Auto finance loans is therefore less about a simple loan button and more about capital efficiency. The attraction is keeping liquidity deployed while accessing borrowed funds. The tradeoff is a position with multiple moving parts: AMM exposure, managed strategy choices, collateral limits, repayment timing, and liquidation rules. Users who understand those parts read the loan offer with clearer expectations and make better use of automated DeFi liquidity management.

Auto finance loans questions worth asking

Can stablecoin LP collateral reduce liquidation risk on Auto finance loans?

Stablecoin LP collateral reduces price volatility compared with volatile token pairs, so the collateral value is easier to monitor. It still carries smart contract, stablecoin, oracle, and pool liquidity risk. The lower volatility also means yields are frequently less dramatic than new-token pools. The loan limit and collateral buffer remain important even when both assets in the pool target stable value.

Which assets fit best with LP-backed DeFi borrowing?

Deep liquidity assets fit this structure better than thinly traded tokens. Stablecoin pairs, ETH pairs, and BTC-linked pairs give the borrower more reliable pricing and exit routes than small pools with weak volume. The chosen assets should match the borrower's repayment asset and risk tolerance, because LP collateral changes composition as pool prices move.

What costs affect an Auto finance loans position besides the borrow rate?

The borrow rate is only one part of the cost. A position also reflects network transaction fees, possible strategy performance fees, swap costs when entering or exiting a pool, and the effect of impermanent loss on the LP collateral. Rewards and trading fees offset some expenses when pool activity is strong, but the borrower should compare total position value with the debt balance.

Do I need to manage the liquidity range myself for Auto finance loans?

The point of a managed LP strategy is to handle range selection, rebalancing, and position maintenance through automated liquidity management. The borrower still chooses the strategy, supplies the needed assets, reviews the loan terms, and monitors collateral health. Automation handles operational adjustments, while the user remains responsible for debt size, repayment timing, and the risk level of the selected pool.